Joint Science Academies' Statement: Energy Sustainability and Security g8

The g8 Joint science academies have released the outline for the global situation and the security of the energy complex for sustainability, innovation,and development.As we have suggested there are a number of interesting developments ,that will see a mix of new technology,efficiency and evolution of existing technology.

Broad international consensus recognizes three principal, inter-related components of sustainable development: economic prosperity, social development, and environmental protection. Sustainable and reliable supply of energy is one of the major conditions for achieving these three goals ,for all countries of the world: if energy sustainability and security fail, the primary human development goals cannot be achieved.

Last year we addressed the major challenges of climate change. These challenges are predominantly related to energy systems and use. We therefore welcome the opportunity to address energy sustainability and security on the occasion of the 2006 G8 Summit - and we expect to continue our focus on these critical issues in future years. The InterAcademy Council, established by the Academies of the world, is now engaged in an in- depth examination of this energy technology transition challenge, to be completed within a year.

Problems and Challenges of Energy Sustainability and Security

It has become increasingly clear that there are very serious difficulties related to sustainability and security of energy. These include:

- Major global and regional impacts on the environment, climate change and health from an extrapolation of current energy sources and systems;

- A clear projection that demand for affordable and clean energy sources will increasingly grow, requiring investments to create an efficient system of global energy supply;

- Tensions, especially in energy supplies for transport systems;

- Increasingly poor geographical correlations between energy sources and users;

- Inefficient and wasteful use of energy resources;

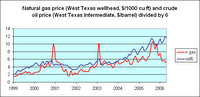

- Sharply rising and fluctuating oil and gas prices;

- Providing fuels and electricity to a significant portion of the world 's population to help improve their quality of life;

- Impacts of natural disasters, systems breakdowns, and human acts on energy infrastructure.

Resolving Energy sustainability and Security Challenges

Providing for global energy sustainability and security will require many vigorous actions at national levels, and considerable international cooperation. These actions and cooperative steps will need to be based on wide- spread public support, especially in exploring venues for increased efficiency of energy use. Secondly, it will be necessary to develop and deploy new sources and systems for energy supply, including clean use of coal and unconventional fossil resources, advanced nuclear systems, and renewable energy. Diversification of engine fuels, increased use of low-emissions technologies in personal transport, and greater emphasis in deployment of urban mass transit would introduce much-needed flexibility and economy in a rapidly urbanizing world.

The necessary changes and transitions in energy systems and paradigms will not be possible without achievement of many challenging scientific, technical and economic objectives, and will require the investment of enormous resources in a sustained way over decades. They will also require major openness and transfer of knowledge, technology and capital.

Achieving an acceptable level of global energy sustainability and security will therefore require sustained governmental focus and international cooperation on identifying strategic energy policy priorities, and the sustained implementation of corresponding policies, actions, and national investments. It will also be critical to involve the public and industry leadership in setting and achieving the key priorities, if we are to collectively deal with threats to energy sustainability and security in time to avoid major economic, environmental, and political damage.

The common strategic priorities should include:

- Promotion of energy efficiency, including improving the energy efficiency and economic effectiveness of the energy system in a holistic way;

- Diversification of energy supply and demand, as diversity of energy mix, sources, markets, transportation routes and means of transportation decrease vulnerability related to single or predominant sources and systems;

- Development of global energy infrastructure with attention to its resilience;

- Promotion of clean and affordable energy sources and systems, including advanced nuclear technologies and renewable systems;

- Decentralization of energy production through development of local energy resources and systems;

- Promotion of cost-effective economic instruments that can help to reduce the emission of greenhouse gases;

- Addressing the urgent human needs of approximately a third of the world population which does not have access to modern energy

Innovation, Research, Development and Deployment

We recognize the special responsibility of the science and engineering community to help implement transitions to sustainable and secure energy systems. We take special note of the areas in which international cooperation, substantial research and development, and innovation, will be critical. Important examples of such areas are:

- Energy efficiency for buildings, devices, motors, transportation systems and in the energy sector itself, which has a great capacity for boosting energy efficiency;

- Systems analysis to find efficient strategies for various conditions; - Clean coal systems, including potential for sequestering of CO2;

- Advanced nuclear systems, addressing the problems of safety, waste, and non-proliferation;

- Pollution control;

- Unconventional fossil fuels and related environmental protection;

- Biomass production and conversion, gas-to-liquid conversion;

- Renewable energy sources for the long-term, such as geothermal, wind, tidal and solar, and energy storage technologies;

- Small decentralized systems addressing needs of poor, rural, and isolated systems, and examination of wider application of such systems.

Conclusions

We call on all countries of the world to cooperate in identifying common strategic priorities for sustainable and secure energy systems, and in implementing actions toward those strategic priorities. G8 countries bear a special responsibility for the current high level of energy consumption, and should play a leading role in assuring global energy sustainability and security.

We call on world leaders, especially those meeting at the G8 Summit in July 2006, to:

- Articulate the reality and urgency of global energy security concerns;

- Plan for the massive infrastructure investments, and lead times required for a transition to clean, affordable and sustainable energy systems;

- Itensify cooperation with developing countries to build their domestic capacities to use existing and innovative energy systems and technologies, including transfer of technologies;

- Promote by appropriate policies and economic instruments the development and implementation of cost-competitive, environmentally beneficial, and market acceptable clean fossil, nuclear, and renewable technologies;

- Ensure, in cooperation with industry, that technologies are developed and implemented and actions taken to protect energy infrastructures from natural disasters, technological failures, and human actions;

- Address the serious inadequacy of R&D funding and provide incentives to accelerate advanced energy-related R&D, also in partnership with private companies;

- Implement education programs to increase public understanding of energy challenges, and to provide for energy-related expertise and engineering capabilities;

- Focus governmental research and technology efforts on energy efficiency, non-conventional hydrocarbons and clean coal with CO2 sequestration, innovative nuclear power, distributed power systems, renewable energy sources, biomass production, biomass and gas conversion for fuels.

Eduardo Krieger - Academia Brasileira de Ciencias, Brazil

Patricia Demers - Royal Society of Canada, Canada

Yongxiang Lu - Chinese Academy of Sciences, China

Edouard Brezin - Academie des Sciences, France

Volker ter Muelen - Deutsche Akademie der Naturforscher Leopoldina, GermanyR.A. Mashelkar - Indian National Science Academy, India

Giovanni Conso - Accademia Nazionale dei Lincei, Italy

Kiyoshi Kurokawa - Science Council of Japan, Japan

Yuri Osipov - Russian Academy of Sciences, Russia

Robin Crewe - Academy of Science of South Africa, South Africa

Martin Rees - Royal Society, United Kingdom

Ralph Cicerone - National Academy of Sciences, United States of America

The g8 Joint science academies have released the outline for the global situation and the security of the energy complex for sustainability, innovation,and development.As we have suggested there are a number of interesting developments ,that will see a mix of new technology,efficiency and evolution of existing technology.

Broad international consensus recognizes three principal, inter-related components of sustainable development: economic prosperity, social development, and environmental protection. Sustainable and reliable supply of energy is one of the major conditions for achieving these three goals ,for all countries of the world: if energy sustainability and security fail, the primary human development goals cannot be achieved.

Last year we addressed the major challenges of climate change. These challenges are predominantly related to energy systems and use. We therefore welcome the opportunity to address energy sustainability and security on the occasion of the 2006 G8 Summit - and we expect to continue our focus on these critical issues in future years. The InterAcademy Council, established by the Academies of the world, is now engaged in an in- depth examination of this energy technology transition challenge, to be completed within a year.

Problems and Challenges of Energy Sustainability and Security

It has become increasingly clear that there are very serious difficulties related to sustainability and security of energy. These include:

- Major global and regional impacts on the environment, climate change and health from an extrapolation of current energy sources and systems;

- A clear projection that demand for affordable and clean energy sources will increasingly grow, requiring investments to create an efficient system of global energy supply;

- Tensions, especially in energy supplies for transport systems;

- Increasingly poor geographical correlations between energy sources and users;

- Inefficient and wasteful use of energy resources;

- Sharply rising and fluctuating oil and gas prices;

- Providing fuels and electricity to a significant portion of the world 's population to help improve their quality of life;

- Impacts of natural disasters, systems breakdowns, and human acts on energy infrastructure.

Resolving Energy sustainability and Security Challenges

Providing for global energy sustainability and security will require many vigorous actions at national levels, and considerable international cooperation. These actions and cooperative steps will need to be based on wide- spread public support, especially in exploring venues for increased efficiency of energy use. Secondly, it will be necessary to develop and deploy new sources and systems for energy supply, including clean use of coal and unconventional fossil resources, advanced nuclear systems, and renewable energy. Diversification of engine fuels, increased use of low-emissions technologies in personal transport, and greater emphasis in deployment of urban mass transit would introduce much-needed flexibility and economy in a rapidly urbanizing world.

The necessary changes and transitions in energy systems and paradigms will not be possible without achievement of many challenging scientific, technical and economic objectives, and will require the investment of enormous resources in a sustained way over decades. They will also require major openness and transfer of knowledge, technology and capital.

Achieving an acceptable level of global energy sustainability and security will therefore require sustained governmental focus and international cooperation on identifying strategic energy policy priorities, and the sustained implementation of corresponding policies, actions, and national investments. It will also be critical to involve the public and industry leadership in setting and achieving the key priorities, if we are to collectively deal with threats to energy sustainability and security in time to avoid major economic, environmental, and political damage.

The common strategic priorities should include:

- Promotion of energy efficiency, including improving the energy efficiency and economic effectiveness of the energy system in a holistic way;

- Diversification of energy supply and demand, as diversity of energy mix, sources, markets, transportation routes and means of transportation decrease vulnerability related to single or predominant sources and systems;

- Development of global energy infrastructure with attention to its resilience;

- Promotion of clean and affordable energy sources and systems, including advanced nuclear technologies and renewable systems;

- Decentralization of energy production through development of local energy resources and systems;

- Promotion of cost-effective economic instruments that can help to reduce the emission of greenhouse gases;

- Addressing the urgent human needs of approximately a third of the world population which does not have access to modern energy

Innovation, Research, Development and Deployment

We recognize the special responsibility of the science and engineering community to help implement transitions to sustainable and secure energy systems. We take special note of the areas in which international cooperation, substantial research and development, and innovation, will be critical. Important examples of such areas are:

- Energy efficiency for buildings, devices, motors, transportation systems and in the energy sector itself, which has a great capacity for boosting energy efficiency;

- Systems analysis to find efficient strategies for various conditions; - Clean coal systems, including potential for sequestering of CO2;

- Advanced nuclear systems, addressing the problems of safety, waste, and non-proliferation;

- Pollution control;

- Unconventional fossil fuels and related environmental protection;

- Biomass production and conversion, gas-to-liquid conversion;

- Renewable energy sources for the long-term, such as geothermal, wind, tidal and solar, and energy storage technologies;

- Small decentralized systems addressing needs of poor, rural, and isolated systems, and examination of wider application of such systems.

Conclusions

We call on all countries of the world to cooperate in identifying common strategic priorities for sustainable and secure energy systems, and in implementing actions toward those strategic priorities. G8 countries bear a special responsibility for the current high level of energy consumption, and should play a leading role in assuring global energy sustainability and security.

We call on world leaders, especially those meeting at the G8 Summit in July 2006, to:

- Articulate the reality and urgency of global energy security concerns;

- Plan for the massive infrastructure investments, and lead times required for a transition to clean, affordable and sustainable energy systems;

- Itensify cooperation with developing countries to build their domestic capacities to use existing and innovative energy systems and technologies, including transfer of technologies;

- Promote by appropriate policies and economic instruments the development and implementation of cost-competitive, environmentally beneficial, and market acceptable clean fossil, nuclear, and renewable technologies;

- Ensure, in cooperation with industry, that technologies are developed and implemented and actions taken to protect energy infrastructures from natural disasters, technological failures, and human actions;

- Address the serious inadequacy of R&D funding and provide incentives to accelerate advanced energy-related R&D, also in partnership with private companies;

- Implement education programs to increase public understanding of energy challenges, and to provide for energy-related expertise and engineering capabilities;

- Focus governmental research and technology efforts on energy efficiency, non-conventional hydrocarbons and clean coal with CO2 sequestration, innovative nuclear power, distributed power systems, renewable energy sources, biomass production, biomass and gas conversion for fuels.

Eduardo Krieger - Academia Brasileira de Ciencias, Brazil

Patricia Demers - Royal Society of Canada, Canada

Yongxiang Lu - Chinese Academy of Sciences, China

Edouard Brezin - Academie des Sciences, France

Volker ter Muelen - Deutsche Akademie der Naturforscher Leopoldina, GermanyR.A. Mashelkar - Indian National Science Academy, India

Giovanni Conso - Accademia Nazionale dei Lincei, Italy

Kiyoshi Kurokawa - Science Council of Japan, Japan

Yuri Osipov - Russian Academy of Sciences, Russia

Robin Crewe - Academy of Science of South Africa, South Africa

Martin Rees - Royal Society, United Kingdom

Ralph Cicerone - National Academy of Sciences, United States of America

posted by maksimovich | 3:11 PM

|

0 comments

![]()

![]()